Why Wall Street is Wrong About Blue Owl ($OWL)

On the SaaSpocalypse, the private credit panic, and more

Alternative asset managers have taken a beating over the past year. The selling traces to two fears: that private credit is quietly unwinding, and that AI will gut the software companies these firms lend to. Several quarters later, the numbers haven’t really shown up to support them. The most punished, Blue Owl Capital, is still down more than half from its high, the steepest drop in the group. So Blue Owl is the case worth studying, because the gap between the story and the numbers is widest there.

As my analysis will show, the two fears were broad and abstract until Blue Owl did something that made it the market’s scapegoat for both. After that, the stock fell much further than the business did, and that gap is the contrarian opportunity.

Let’s start with Blue Owl’s most recent quarter’s results:

Fee-related earnings up at a healthy double-digit clip.

Assets under management up to $315 billion, fifteen percent higher than a year ago.

$11 billion of new capital raised, two-thirds of it institutional.

Management buying back its own stock at these prices.

Small negative return in the direct lending platform, mostly driven by spread widening and mark-to-market movements.

Blue Owl trades at about $10 today. It went public through a SPAC, and SPACs go public at $10. So you can own the company at the same price it fetched five years ago. Back then it managed about $52 billion in assets. Today it manages $315 billion, its fee earnings per share have more than doubled, and it pays a dividend now yielding near nine percent.

Almost everyone believes in some form of market efficiency, so let’s understand what story the market is telling itself, and whether the story holds when you trace it carefully.

The two fears, and the catalyst that made them Blue Owl’s

The bear case is not one fear but two, and a third thing that is not a narrative at all but an event.

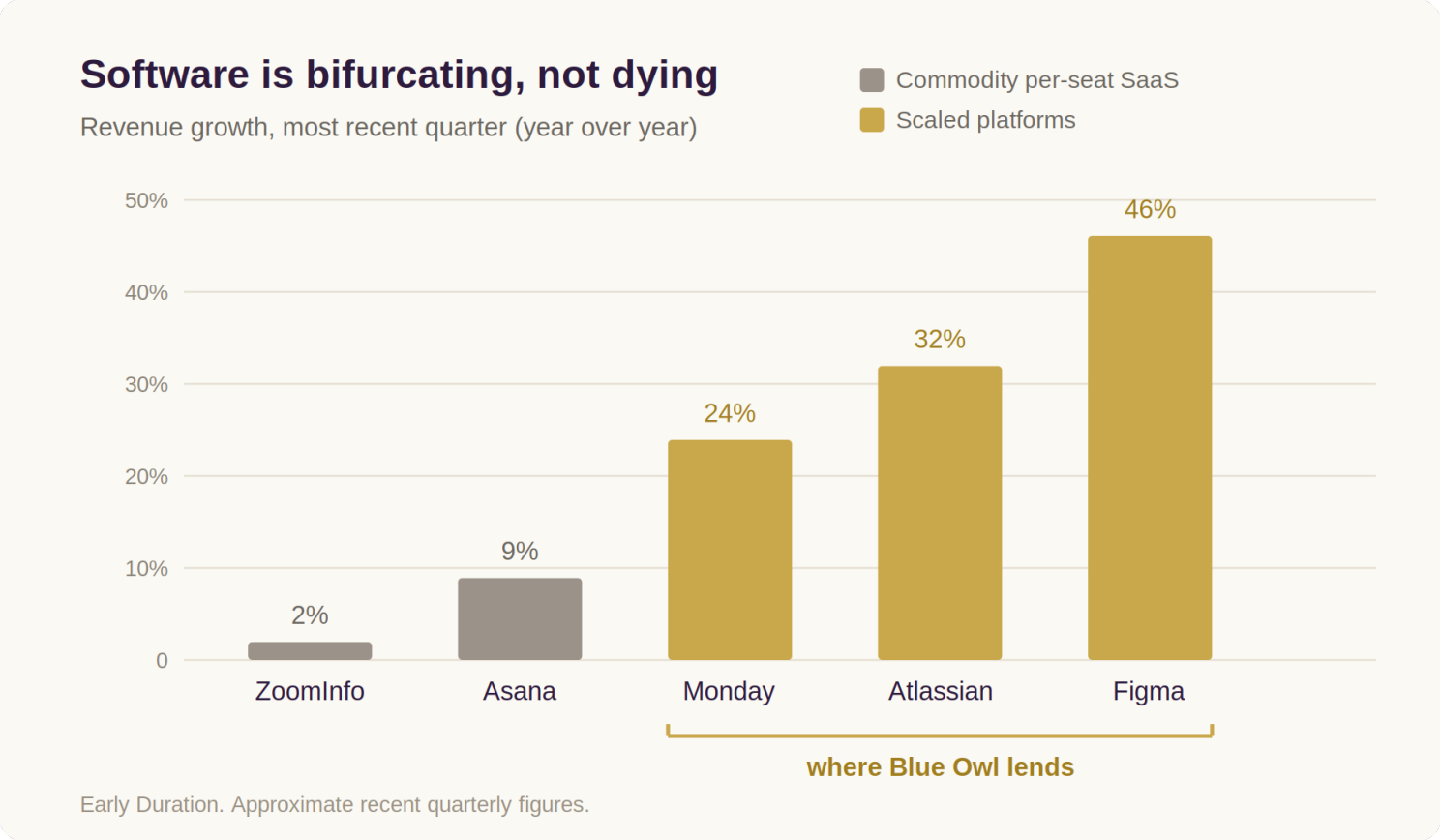

The first fear is the SaaSpocalypse. The acceleration of agentic AI tooling earlier this year erased something on the order of a trillion dollars from software valuations on a single thesis: per-seat pricing only works when seats expand, and if AI agents collapse the number of seats a company needs, the terminal value math breaks. Blue Owl, through its technology lending platform, is among the largest non-bank lenders to software companies in the world, so the story found it quickly.

The second fear is the broader private credit panic, building since the First Brands and Tricolor frauds last fall and cresting when Blue Owl capped redemptions on two of its largest non-traded funds. One vehicle saw tender requests for more than forty percent of its shares. The firm paid out the contractual maximum, but the press wrote about it as if a door had been slammed shut, and the alternative managers have struggled to explain to the public why their portfolios are more resilient than the headlines suggest.

The third thing is an event: late last year, Blue Owl scrapped a planned merger of its unlisted credit BDC into its listed one, citing market conditions. The unlisted fund’s holders had realized that the merger would have repriced their interests to the listed vehicle’s traded level, implying a markdown on the order of twenty percent. So people protested and, in addition, fund withdrawals were frozen in the process of closing, which rattled shareholders trying to exit. This event gave the market a Blue Owl-specific reason to believe that Blue Owl’s marks, Blue Owl’s liquidity, and Blue Owl’s franchise were more fragile than the peer group’s, and that differential has carried ever since.

The SaaSpocalypse

Robert Shiller often argues that markets move less on fundamentals than on the contagious stories investors tell each other about them, and the SaaSpocalypse is a textbook specimen: a vivid, transmissible story that traveled faster than the data on how customers were actually behaving. The story is not wrong, in fact, I believe it is exactly right about a specific slice of software. Undifferentiated per-seat tools whose entire moat was a sticky login are being repriced because they should be.

However, the same productivity wave threatening commodity software is driving the boom in scaled software, because the gains accrue to the platforms that already own the customer relationship into which AI gets deployed. The interesting cases sit between the doomed mid-tier and the hyperscalers, and they tell you what is happening at the tier where Blue Owl actually lends.

The obvious objection is that these are public companies, a convenient and not quite representative sample, since a public company has greater access to capital markets, where a sponsor-owned borrower carrying buyout debt has less room. I think private software actually adapts better, not worse. A sponsor’s portfolio companies sit side by side and share what works, so a pricing model that succeeds at one spreads quickly to the rest. To me, “quality” in software has become mostly a question of whether a company has already reached scale, and Blue Owl lends to the ones that have. Private borrowers also work more closely with their lenders. The loans are bespoke and bilateral, not broadly syndicated, which avoids the lender-on-lender fights, the so-called “creditor-on-creditor violence”, that have become common in the syndicated market.

Then there is the concentration argument, which is about exposure rather than quality. Blue Owl’s technology fund is roughly 70% software, against something like 26% at Blackstone’s flagship credit fund, 20% at Ares, and 7% at KKR. By the standard of a diversified lender that is an enormous single-sector bet, and the critics who call it a violation of portfolio discipline have a point. What they leave out is that the 70% is the dedicated technology vehicle, a specialist meant to be concentrated in software the way an energy fund is meant to be concentrated in energy. Across the broader platform and the franchise as a whole, software is a normal-sized slice. The market is pricing the entire company as though software were its total risk.

And is software a good thing to concentrate in? For a senior secured lender, it has historically been one of the best. Recurring revenue, asset-light balance sheets, and private equity owners with real money underneath the debt. With AI, it is now easier than ever to ship better software with fewer people, which helps these borrowers more than it hurts them.

The Private Credit Panic

The private credit panic started with First Brands and Tricolor, a real but limited set of failures. We are coming up on a year since, and conditions have not materially worsened. The complaint is that private credit is opaque and the danger is hidden. Fair enough. So take it apart.

Start with losses. Non-accruals across Blue Owl’s funds are running at a small fraction of a percent. The broadest published default index sits below three percent, with software defaults notably absent.

Now grant the obvious objection. Non-accruals understate true distress, because covenant amendments and quiet restructurings keep a struggling borrower technically current. Analysts put the real default rate closer to five percent.

But that distress sits where Blue Owl does not lend. It is concentrated in the lower middle market and the unsponsored bottom, where defaults have breached nine percent. At Blue Owl’s borrower tier, amendments are far more often strategic than a sign of trouble.

The strongest evidence the marks are honest is the roughly $1.4 billion of loans Blue Owl sold early this year. It sold at book value, to four outside pension and insurance buyers, with software the single largest piece. Selling at the carried mark, to sophisticated third parties, shows the marks are fair and achievable. It is not airtight proof, because we do not know how those particular loans were chosen from a much larger book. But outside buyers with their own credit teams paid book for a representative slice, and its biggest exposure was the exact sector the SaaSpocalypse was supposed to have destroyed.

What Blue Owl actually is

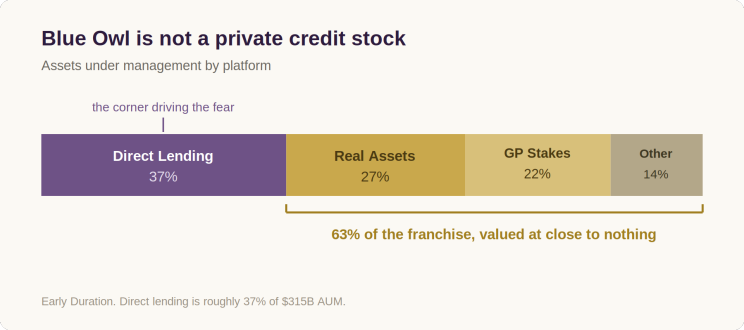

Blue Owl is not a private credit stock. It is an alternative asset manager earning fees across three distinct platforms, and direct lending is only a little over a third of the whole.

The real assets platform is principally net lease and digital infrastructure, long-duration income that benefits directly from the same AI capex cycle the bear case implicitly assumes will continue. The same hyperscaler buildout supposedly killing the software lending book is filling the data center book at unusually wide spreads, and Blue Owl is bidding on infrastructure financings measured in the tens of billions. The GP stakes platform takes minority positions in other alternative managers and dominates the market for large stake transactions, which gives it a perpetual claim on the fees, balance sheets, and carry of the broader industry as it compounds. The market is pricing the entire franchise as if it were the most stressed corner of the loan book.

Historical Analogy

In 2015 and 2016, energy credit fears hammered the same kind of firms. The ones that marked down, waited, and bought into the wreckage were rewarded fast. Within a year the market turned, and energy loans alone returned about forty-five percent. Today rhymes: wider spreads, thinner bank competition, and ample dry powder management can deploy. While Energy has a visible futures market whereas Private Credit is slower and more diffuse, the shape of the opportunity is the same.

What would change my mind

Here are some signals that would cause me to reconsider:

Non-accruals climbing past three percent, or the true default rate at Blue Owl’s tier converging on the five percent estimated for the asset class.

A drop in new commitments, especially recycled money from existing investors rather than new names. Or less interest from wealth advisors.

Amendment activity picking up at Blue Owl’s borrower tier, not just the lower middle market.

Sustained erosion in the fee-related margin, the one metric the franchise premium most depends on.

None of the credit signals has fired. The one flickering is the wealth channel, where redemptions rose and perpetual fundraising slowed, though institutional commitments more than made up the difference. The strongest bear case runs like this:

The marks are stale, because Level 3 valuation lags reality and managers have every incentive to delay markdowns.

First Brands showed that sponsors can hide leverage and inflate EBITDA, so reported borrower health cannot be taken at face value.

Payment-in-kind interest is masking cash-flow stress that will surface when the maturity walls of the next two years arrive.

The forty-percent redemption queue is a permanent buyer’s strike, with the pulled merger as the first crack.

That’s a fair argument, and the answer is already above: the marks cleared at book in an arm’s-length sale, the institutional bid kept coming through the quarter, the redemption math is bounded and covered many times over, and the pulled merger reads more as avoiding a markdown for unlisted holders than as a sign the cash was not there. Two points are worth adding. First Brands was a syndicated-loan situation, lightly governed and built for distribution, where direct loans are bilaterally negotiated, tightly covenanted, and continuously monitored, so the tricks that worked there do not travel. And on PIK, the distinction that matters is origination versus amendment: nearly all of Blue Owl’s was structured at origination as a financing preference of scaled borrowers, not negotiated later under distress, which is the real warning sign and the first place I would expect the thesis to break.

The Trade

The most exposed name in alternative asset management, the one carrying the two loudest fears and the event that gave them a target, has a business that is much more resilient than Wall Street thinks. Fee earnings are still growing and a large pool of committed capital is waiting to deploy. And the credit data sits inside sector norms, even after you grant the bears their best points.

The narrative has been that private credit is broken and software is dead. Several quarters in, I still haven’t seen the numbers to support it. Private credit has taken an unfair beating, and Blue Owl has taken the worst of it.

If the next two quarters show PIK accelerating, the fundraising flywheel reversing, or non-accruals climbing into the threes, then I am wrong and the market saw something I didn’t. Until then, the price is the story, and the story has outrun the data.

Early Duration is a financial newsletter on insurance and financial markets. The prior issue of “Why Wall Street is Wrong” is on YouTube here.