Please, just cockroaches.

A review on how the SaaSpocalypse connects to the life insurance balance sheet

Remember when the only trade against AI was buying credit default swaps on Oracle? Good times. Six months later, we’ve gone up the food chain from cockroaches to Blue Owl. I can only hope we won’t have to discuss a black swan, but Nassim Taleb is as active as ever, Michael Burry started his Substack, and everyone has made it clear that AI’s disruptive nature to software companies may be a sign for what’s to come.

On the defense, we have asset managers who have intimate relationships with both these SaaS companies (which need to be saved from AI) and insurance companies (serving policyholders who need to be saved). Traditionally opaque in the way they operate, they’ve taken a bolder stance these days in defending their positioning: they have multiples of dry powder sitting around compared to their software exposure.

Perhaps they would have drawn less attention if they didn’t push so hard to get private funds into retail hands and 401(k)’s, but then again they are just giving people what they want, which is higher yield and more options.

And so where we’re at in the current discourse is the following:

AI makes software so easy to replicate that SaaS companies face enormous pressure on renewals

Private Equity firms own these companies and many also own insurance companies and pension funds that buy their debt

Insurance and pensions provide financial security, and normal people aren’t familiar with how the tie-up works, so they’re scared

And the PE firms argue that the exposure is not that scary and they can influence anything needed like cost cuts and restructure faster than a standalone company dealing with issues on its own

The defense might be right. But the problem is that nobody is watching the whole chain. Think of this piece like Citrini’s “Global Intelligence Crisis,“ only zoomed in on the forward-looking mechanics specific to insurance.

Here’s the chain I’ve been tracing: AI compresses software revenue → covenants break → lenders grant PIK amendments instead of forcing defaults → stress stays hidden while debt compounds → CLO collateral pools deteriorate → mezzanine tranches get downgraded → capital charges triple → insurers are forced to sell into a secondary market that barely exists for these instruments. The difference between this and a normal credit cycle is that the forced selling is coming from assets that were never supposed to be sensitive to market cycles in the first place.

Where the Chain Starts

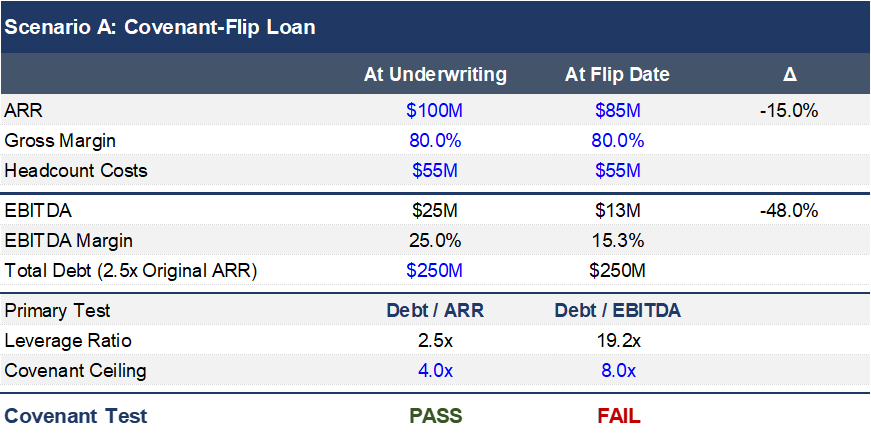

The chain starts with the loans themselves. Several structurally distinct covenant types exist, but the two that matter most are ARR-based and covenant-flip.

ARR-based covenants were designed for high-growth, cash-burning software companies that couldn’t pass an EBITDA test because they were intentionally unprofitable. These loans test against Annual Recurring Revenue, typically at 2x to 4x ARR. This is the critical distinction: when AI compresses a borrower’s revenue, you can’t cost-cut your way back to compliance the way you can with an EBITDA covenant. Revenue is a top-line number so you either have the customers or you don’t.

Covenant-flip loans are the structure I keep coming back to, because they are where the chain’s first real failure point lives. Most ARR loans include a mandatory conversion (typically 24 to 36 months after closing) where the primary test switches from ARR-based to EBITDA-based (as in, the company flipped to becoming profitable). In the below scenario, if revenue shrinks 15% because of AI-related reasons, they will simply fail the test:

The PE Defense

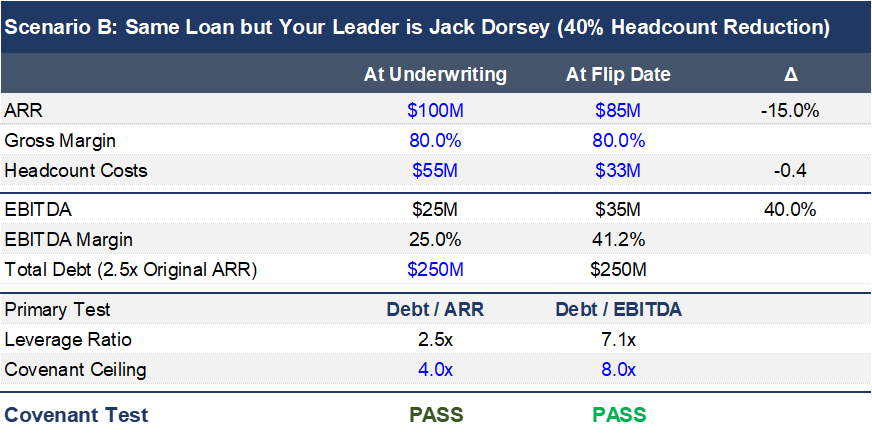

The PE defense, in its strongest form, is genuinely compelling. SaaS businesses have gross margins above 75%, human capital costs are 55% to 65% of revenue, and management can pull the same lever Jack Dorsey (lay off half the workforce) pulled at Block.

Now take a new Scenario B with the same company and the same stress, but with a 40% headcount reduction:

I think the math works. But even ignoring the obvious problems (severance costs, customer flight from a company that just fired 40% of its staff, reputational or legal damage), the thesis has a sequencing problem: restructuring costs hit immediately, savings arrive quarters later, and if the company was already cash-flow negative (approximately 40% of private credit borrowers currently are), it can’t make cash interest payments during the transition. It needs a PIK amendment.

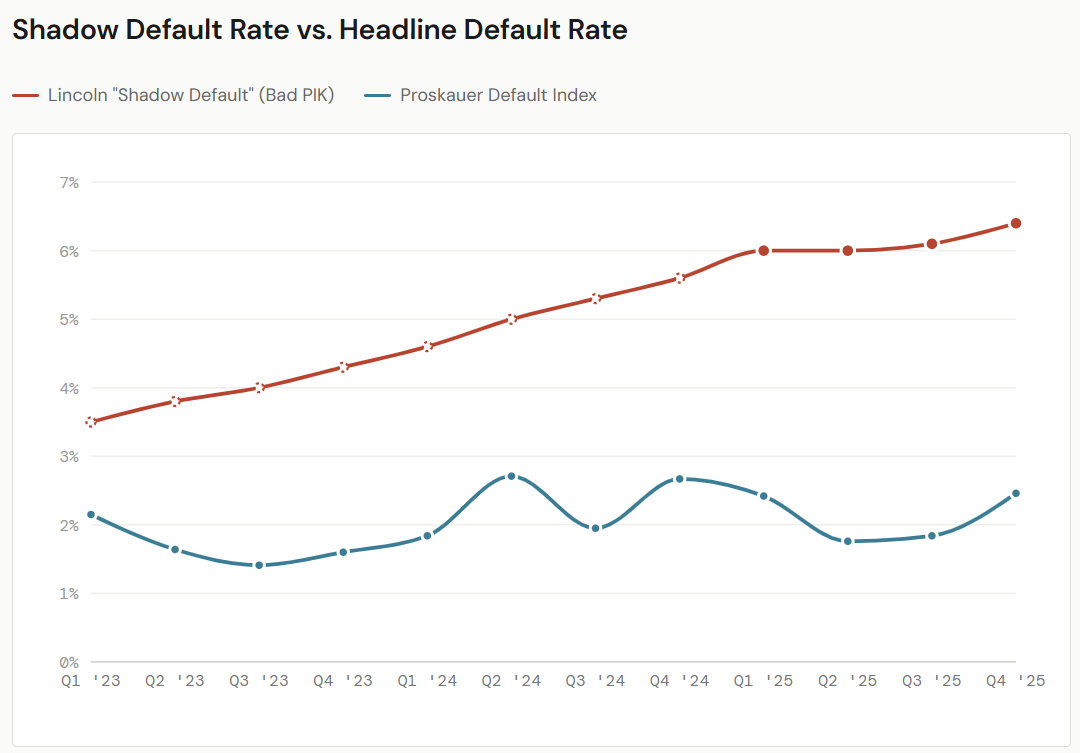

The Shadow Default Rate

Lincoln International tracks a proprietary database of private credit portfolio company performance. Eleven percent of all valued private credit loans now utilize some form of PIK interest, up from 7% in 2021, and more than half of that is what Lincoln classifies as “Bad PIK,” meaning the loan was originally underwritten as cash-pay but the borrower couldn’t make the payments.

To be fair, the ability to restructure without coordinating across dozens of syndicate members is genuinely one of private credit’s structural advantages. But the same flexibility allows lenders to defer loss recognition, because every PIK amendment preserves the appearance of a performing loan and maintains fees on total AUM (which grow as PIK compounds principal). A $100 million loan accruing PIK for two years becomes $108 million in debt against a company worth half what it was at origination. Growing debt and shrinking collateral (and by the way, software assets have a very low recovery rate) means greater exposure.

Blue Owl and the 99.7-Cent Sale

Blue Owl is, across its lending platform, overwhelmingly a software lender (more than 70% of loans, per their Q4 earnings call). In late 2025, redemption requests on its non-traded OBDC II exceeded the 5% quarterly cap. Blue Owl permanently halted redemptions, transitioned OBDC II into run-off, and sold $1.4 billion in loans at 99.7 cents. The buyers were pension funds and an insurance company. The major PE-affiliated asset managers are now down 10% to 30% from recent highs, with the market repricing the sector on events like this where illiquid assets have been forced to look for liquidity.

Why CLOs Are the Bigger Problem

If insurers held software loans directly, this would be a manageable problem. The PE firm can restructure the borrower, grant a PIK amendment, coordinate across its portfolio, or sell the loan outright (which is exactly what Blue Owl did).

But most of the software loan exposure on insurance balance sheets doesn’t sit there as individual loans. It sits inside CLO tranches (collateralized loan obligations, vehicles that buy pools of leveraged loans and issue tranches of debt from AAA to equity against them). And inside a CLO, the PE advantage is sharply diminished. A PE firm can restructure a borrower on their insurer’s direct loan book, but they cannot reach into a CLO tranche and swap out the software collateral. Apollo, KKR, and others do manage CLOs through their credit platforms, which gives them some ability to actively trade the underlying collateral. But even on the self-managed book, they’re constrained by the indenture and owe duties to all tranche holders, not just their affiliated insurer.

For a typical large PE-affiliated life insurer, CLOs can represent 10% to 18% of invested assets (the industry average is ~4%, but PE-affiliated insurers are far more concentrated), and these are the balance sheets backing annuity contracts and pension obligations for tens of millions of Americans.

CLOs are where the chain gets genuinely dangerous, for three reasons.

First, the insurer can’t even see how exposed it is. The true software concentration in CLO collateral pools is masked by how GICS codes classify things (billing software becomes Financial Services, marketing SaaS becomes Media, and suddenly the 10% to 12% industry cap in the CLO indenture actually turns out to be 20%).

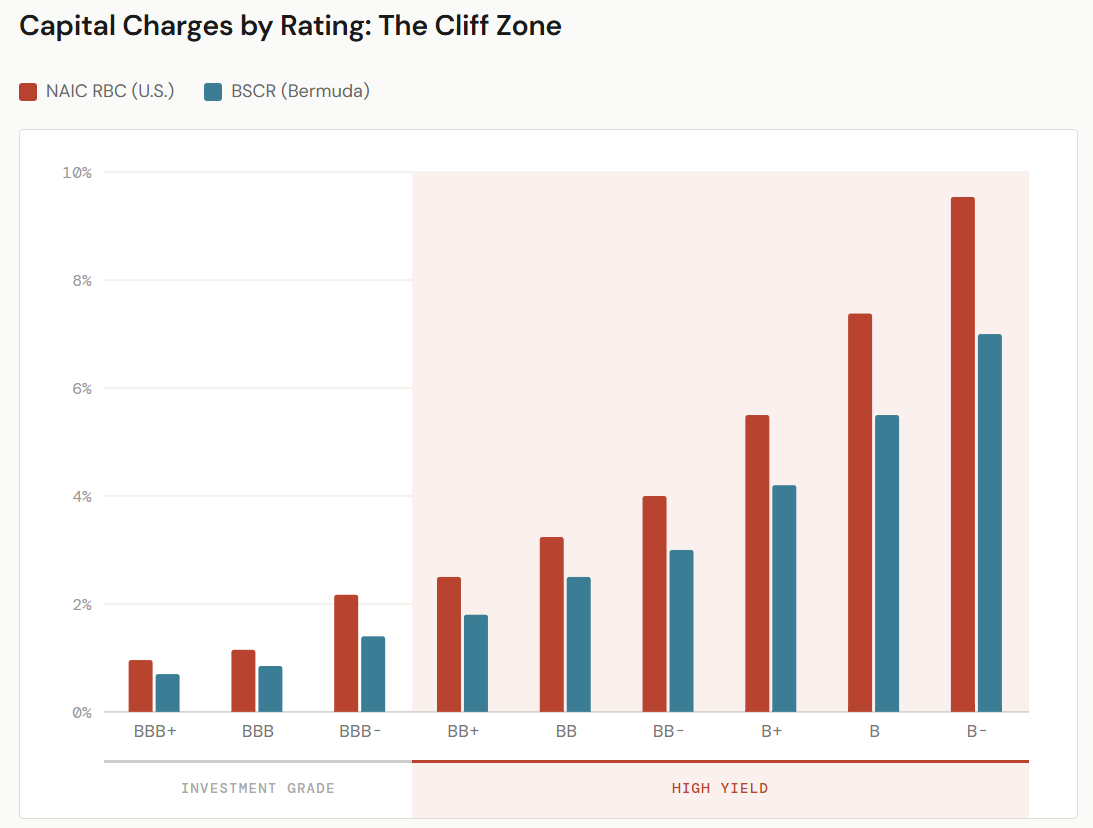

Second, the capital charges escalate quickly. As the chart below shows, capital charges increase exponentially each step down the designation ladder, and the framework was built for gradual migration of a few names at a time, not an entire sector moving at once.

Third, and I think this is the sharpest point: the whole reason insurers held these loans through CLO tranches was to get investment-grade capital treatment on speculative-grade risk. That’s a genuine structural advantage in calm markets. But when ratings migrate, not only do you lose the discount, now you’re stuck with a downgraded asset in an ultra-thin secondary market instead of a loan you could have restructured or sold off.

When enough software loans experience PIK amendments or defaults, the cascade runs: CCC buckets breach a 7.5% threshold → Overcollateralization tests fail → CLO waterfalls divert cash from mezzanine → rating agencies downgrade → capital charges triple.

The natural objection is that software is only 15% to 20% of the collateral pool. Why would stress in one sector blow up the structure? Because CLO mezzanine tranches sit right at the edge of their structural tolerances, and those tolerances assume diversified, uncorrelated defaults: a borrower here, a borrower there. Sector-wide stress is different and if AI hits all SaaS simultaneously, you can breach the 7.5% CCC bucket with stress in just that one sector. Once the OC tests fail, the mezzanine tranche loses its coupon, which changes expected recovery, which triggers the downgrade.

A composite PE-affiliated life insurer starts at a 400% Risk-Based Capital ratio. AllianceBernstein estimated that the NAIC’s new CLO capital framework alone could reduce the average life insurer’s RBC ratio by 10 to 20 points, and that’s at the industry-average 4% CLO allocation. PE-affiliated insurers with three to five times that concentration would face a proportionally larger hit, before you even add software-driven ratings migration on top.

The Ratings Trap

Okay, so a drop from 400% to 350% RBC is bad, but it’s still way higher than any regulatory threshold. What gives? AM Best, S&P, Fitch, and Moody’s, whose capital adequacy models are far more conservative than NAIC minimums, would be the punishers here. An A+ financial strength rating (which an insurer needs to win pension risk transfer business) requires capital well in excess of regulatory floors. A drop to 350%, combined with a portfolio that now contains meaningfully more NAIC-3 and NAIC-4 securities, triggers a negative outlook from AM Best. And a single-notch downgrade from A+ to A severely punishes an insurer competing for pension mandates or financing through funding agreements.

The insurer now faces a choice between two bad options. It can sell the downgraded CLO tranches into a secondary market that can barely absorb normal volume. Or it can hold them, absorb the tripled capital charges, and either accept the ratings downgrade or get the PE parent to recapitalize, at the exact moment the parent’s own stock is down and its LPs are asking about software exposure. And if multiple PE-affiliated insurers need the same injection simultaneously, the capital demand is correlated in exactly the way the original allocation assumed it wouldn’t be.

The incentive structure pushes toward selling. CLO mezzanine tranches hitting the market at the same moment every similarly positioned insurer faces the same pressure. Prices drop, mark-to-market losses hit other holders, their own rating reviews begin. The selling causes more downgrades, which causes more selling.

The Federal Reserve flagged the setup in its March 2025 FEDS Note: life insurers’ exposure to sub-investment-grade corporate debt now exceeds their exposure to subprime RMBS in late 2007. And over $1 trillion in reserves have been ceded to Bermuda, which operates under different capital rules (BSCR) with less visibility into actual holdings; but as the chart shows, BSCR charges increase non-linearly on downgrades in the same way NAIC charges do.

Please, Just Cockroaches.

The original cockroaches, the ones Jamie Dimon was referring to, were Tricolor and First Brands: both fraud cases rather than some systemic worry like AI, and both came from the traditional lending system. Since the highly regulated banking sector couldn’t catch Tricolor double-pledging collateral for seven years, there’s valid reason for concern in the more opaque private markets. If we do end up having issues, the scenario doesn’t need to be dramatic. A software squeeze followed by CLO contagion may be how we see an insurance fallout, but as long as it’s just a few cockroaches and doesn’t spread up the food chain, forced selling should stay contained.

The cockroaches everyone is looking at came from outside private credit. The chain I’m worried about runs through it, from software to covenants to CLOs to the pension fund that owns it. Everyone else in this chain can act. The PE firm can restructure, the CLO manager can trade, the fund investor who smelled trouble at Blue Owl could redeem. The retired teacher whose pension made those allocations can’t. She didn’t choose this exposure, she can’t see it, and while regulators and courts are watching (the AT&T pension lawsuit is one of several), no single one of them has visibility across the whole chain.